Governance

A REVIEW OF CORPORATE

GOVERNANCE PROPOSALS

IN FINANCIAL INSTITUTIONS

It is accepted in finance

assessing worth in terms of cash.

Appraisals show how things are worth

and we can state that figures talk.

Pricing is the nature of finance. Expected benefits from business

strategy are estimated by the net present value of investment

opportunity. However, events of recent few years intensified

assessment of losses caused by the Global Financial Crisis.

Nowadays, many countries combat with the economic recession

caused by the financial crisis. Banks and financial institutions

launched huge and quick profit strategies and share-out great

compensations from the superior performance. However, this

short term sight and risk underestimation hit the oldest and largest

financial institution in the world. The Global Financial Crisis woke up

safeguards of sustainability and highlighted entrenched problems

in corporate governance.

What are managers� intentions and what is the aim of the boards?

Are managers� actions hidden, or simply, the boards are blind?

Maybe authority failed? Questions regarding the principal-agent

problem and moral hazard intensified international organizations

to share good governance practices and work alongside

the improvements of corporate governance standards.

This review will look at the recent proposals to handle

the principal-agent problems that exist in financial institutions by

learning from the OECD reports[1] on global findings and key

messages associated with corporate governance and the financial

crisis, examining practices of corporate governance in six US banks[2]

and 25 largest European banks[3] and analysing UK government�s

initiatives[4] and other complementary actions to enhance corporate

governance standards.

Principal-agent problems arise from the separation of ownership and control in a company. �Managers have little incentive to work in the interests of the shareholders when this means working against their own self-interest�[5]. Thus, the role of corporate governance is minimizing conflicts of interest through control systems, regulations and incentives.

The boards represent shareholders. However, the effect of monitoring management team through the boards is limited.

Agency costs mainly are caused by management entrenchment. It occurs when managers do not feel a threat of dismissal and run the business in their own best interest. These costs arise particularly in company�s where ownership is diluted and managers have sufficient large share holdings. Managers benefit themselves at the expense of shareholders by their powerful influence on decisions. In this instance, autocracy destroys company�s long term value maximization.

Examples of agency costs include declined managers� efforts to work productively, increased their temptations for excessive spending on perks, misleading decisions regarding necessary capital expenditures or inefficient fund allocation.

Thus, it is expected that independent directors represent shareholders� interests better. But independency may also be destroyed by long term CEO�s tenure. As long as the board starts supporting CEO�s position rather than shareholders, it is said that the board is captured.

The same agency costs arise due to the double CEO/Chairman position. In this case, management entrenchment increase and control is violated. Thus, separated roles of the CEO and the Chairman may prevent from moral hazard.

Additionally, as boards evaluate business strategy, control the use of capital and monitor managers� performance, a company�s wealth is highly depends on their responsibility and competence. Thus, in order the board�s duties were implemented efficiently and agency problems were eliminated, the members of the board should be aware of the shareholders rights and interest. Moreover, directors should understand how risks could be managed and long-term business value is maximized.

According to the OECD reports on corporate governance, it was acknowledged that perfect regulations cannot be prepared. However, some key suggestions regarding good board practices may be valuable.

Lessons from the financial crisis forced to rethink the importance of objectivity and independency in decision making as well as emphasised the significance of directors� professional skills. It was noticed that impartiality is highly expected from non-executive directors. Thus, quality of decisions could be raised as long as required capacities for non-executive directors are clearly identified and their proficiency is permanently developed.

The other considered aspect of efficiency was the equilibrium of power within board members. So, separation of the CEO/Chairman role was particularly emphasized as a necessary condition for healthy debate.

Additionally, monitoring of boards� efficiency was greatly encouraged for the purpose of increased transparency and productivity of corporation�s performance.

1.3. A review of board practices in US and European banks

Following the outline of key findings regarding the good board practices let�s examine, whether these considerations are relevant to the banking sector. Thus, the implications of independency, financial industry expertise, board practices and diversity on banks� performance will be estimated next.

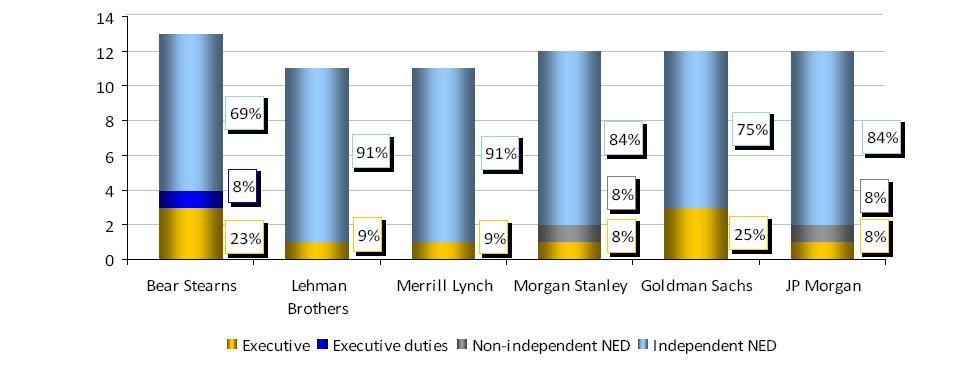

According to the case study of the six US investment banks, the proportion of independent board members of the peer group was substantially higher than executives (see Figure 1). Moreover, it is a common practice in US.As a result, we may suppose that non-executive directors knew little about the affairs of the corporation. Thus, they were lack of managerial oversight that led to the fewer executives� accountability to shareholders.

Figure 1: Director�s classification in 2007[6]

The contrary practice dominated in Europe. For example, the UK Combined Code states that �The board should include a balance of executive and non‐executive directors (and in particular independent non‐executive directors) such that no individual or small group of individuals can dominate the board�s decision taking�.[7]

As the research showed, all the leaders of the analysed six US banks held combined the CEO/Chairmen roles until the crisis and this is the other aspect of undermined independency. Double CEO/Chairmen role was also the prevailing practice in US. Only recently corporations start separating the CEO/Chairmen role.

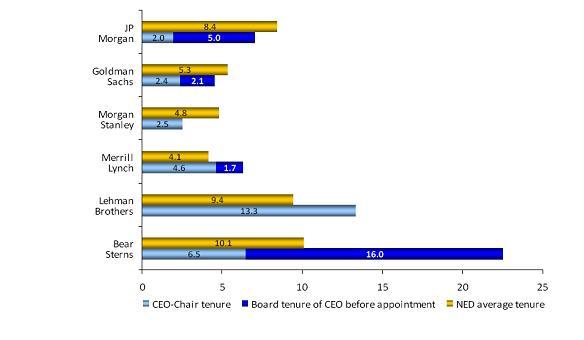

In addition, the CEO/Chairman entrancement of the six US banks was perfectly illustrated by the average tenures of Chairman and the NEDs(see Figure 2). The CEO/Chairman tenures of departed banks (the MER, the LEH, and the BS) were longer compared to the non-executive directors. So, the following outcome may be stated: �Unbroken board tenure of the departed leaders is on average over nine years longer than their peers strongly indicate that �independence of mind� may have been critically absent in the boards of the MER, the LEH and the BS�[8]

Figure 2: Chairman and average NED tenures[9]

Contrary to the US practices, �the UK Combined Code and most European Governance Codes (and, in several cases, laws) suggest that the CEO/Chairman separation is key for the maintenance of appropriate checks and balances within the institution.�[10]

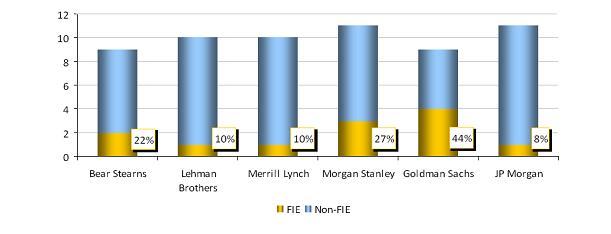

Study of the six US banks also discovered the weak NEDs� capacities to understand issues of rapidly growing financial industry. Figure 3 illustrates that the NEDs did not have sufficient experience to monitor one of the most sophisticated business.

Figure 2: Financial industry experts as a percentage of the NEDs in 2007[11]

As the best practices in Europe showed, when the independency due to the long NED�s tenure is concerned versus his knowledge and experience, the expertise in banking industry appears to be more valuable.

A research about financial industry experience in the 25 largest European banks made in 2008 revealed that 28 % of the NEDs, on average, are competent to solve financial issues. Moreover, interviewed European banks identified that the boards spent most of their time by �questioning and refining company strategy and defining the company�s risk appetite�.[12] The interviewees were also united according the main board�s functions such as �give its approval to acquisitions, joint ventures, disposals, investments or other transactions where such projects were likely to have a �material� impact on the company�s earnings, balance sheet structure, or risk profile�.[13]

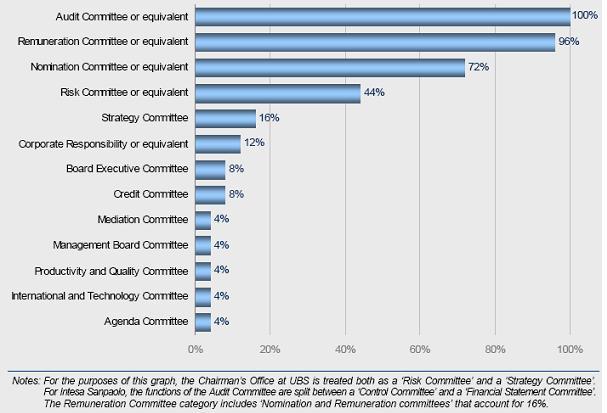

The study of the 25 largest European banks also investigated how decisions are approved. Boards of the European banks usually tackle problems by discussing them in established board committees. Figure 4 illustrates the prevalence of board committees.

Figure 3: The prevalence of board committees (% of peer group with a particular committee)[14]

It appears that all banks have Audit Committee and the biggest part of them set up the Remuneration, the Nomination and the Risk committees. According to the survey, the most active was Audit committee, which held �7.7 meetings a year on average, followed by the Remuneration committee (5.3 meetings a year) and the Nomination committee (4.6 meetings a year).�[15]

The research also revealed that corporate governance issues typically were considered in the Nomination Committee. Moreover, five of the banks had allocated monitoring of changes in corporate governance in the Governance Committee.

As it is stated in the study of the 25 largest European banks, the Audit Committees �(with one exception) are composed exclusively of non-executives. However, only in 16 of these banks is the Audit Committee (in line with international best practice) composed exclusively of independent directors.�[16] The same research showed that there were, on average, 76% of independent NEDs in the Nomination Committee.

Corporate governance investigation in European banks also disclosed the increase of time that the NEDs committed to work in committees. �At Barclays, for example, the minimum commitment level for non-executive directors is 25 days per annum. On top of this, the chairs of the Nomination and Risk Committees are expected to work an additional 11 days. And the chairs of the Audit and the Remuneration Committees are expected to work an additional 25 days.�[17]

Going back to the US practice there was noticed that the NEDs of the GS attended all the committees. This decision is presumed as a good practice that enables the NEDs to broaden their views and raises awareness of comprehensive business. Moreover, it increases better understanding of issues and facilitates decision making.

Furthermore, investigation made in the European banks revealed that a secretary of the companies played important role in serving the board committees and that better forward planning of board sessions increases boards� work efficiency. Moreover, non-executive directors were encouraged to visit regularly business units and communicate with top managers. Such practises enhance productivity and facilitate executive succession planning.

In addition, diversity is also concerned as a good corporate governance practice. Studies showed that board of directors� age, spread of nationalities and gender make balance between the power of leaders and influence substantially on the corporations� performance.

According to the study of six US banks, the following was noticed: age of the board of directors might be a risk factor of the banks� failure. The motive of this statement proposes that older directors are less employable and flexible to meet business challenges.

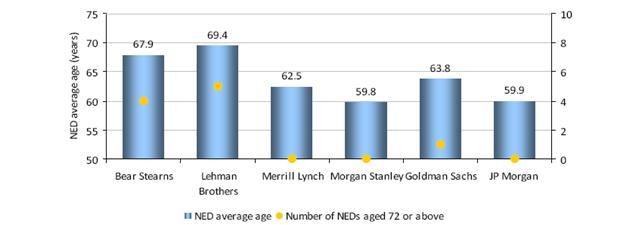

Analysis showed that all the banks those survived (the MS, the GS, and the JPM) along with MER had age limits regarding board membership. The limits of 70-72 years were set in their corporate governance guidelines. Figure 5 illustrates that �the departed board directors were on average 66.5 years old while those of the survivors are 61. Moreover, the BS and the LEH respectively had four and five directors aged above 72 on their board in the departed group, whereas it was uncommon for the survivors to have any�.[18] Studies in European banks disclosed that the NED�s average age is 60 which similar to the survivors of US banks.

Figure 4: Average NED age in 2007[19]

After a review of the OECD reports on corporate governance and the financial crisis as well as findings from the studies of the six US and 25 largest European banks, recent proposals regarding board practices in UK financial institutions will be analyzed.

According to the Walker Review the following distinctive proposals may be mentioned.

Recommendations for better corporate governance in financial institutions emphasize the value of intangible assets: skills, experience, knowledge and objectivity of NEDs. Thus, it was recommended that FSA should be obliged to keep an eye on boards� efficiency by assessing the independency, experience and behaviour of non-executive directors.

It was also noticed that efficiency rises from refreshed board membership and continuity of the firm�s performance. So, recommendation for the Chairman�s (and maybe all board members) annual re-election was stated. Re-election of the Chairman could strengthen his accountability to shareholders. However, simultaneous re-election of all board members may have negative implications on continuity of the firm�s performance.

As it is expected, that efficiency is achieved through the NEDs� competence to make strategic decision, the suggestions for the NEDs� smooth induction and personal training were proposed. Moreover, recommendations took into account the Chairman�s leadership capacities and his ability to encourage effective communication and discussions regarding risk and strategy.

In addition, it was proposed to increase time commitment and work contribution for the Chairman and non-executives in order they were informed better about the company�s affairs.

Principal-agent problems very often intensify when a company faces financial distress. In this instance, the conflict of interest between shareholders and debt holders intensifies.

When a firm is close to bankruptcy, shareholders tend to invest in risky projects. Shareholders know that they will lose their invested money if they do nothing. Moreover, they expect that if a risky project succeeds the company has a chance to survive. However, most of aggressive strategies have a negative NPV, so their implementation destroys company�s value. This shareholders� behaviour is called over-investment problem.

When a firm is close to bankruptcy, shareholders may also do not have incentives to invest in positive NPV projects. This passive position is costly for debt holders because missed positive investment opportunities destroy company�s value as well. This shareholders� behaviour is called under-investment problem.

Moreover, companies that face financial distress have incentives to withdraw money instead of investing it. Shareholders may be encouraged to sell existing tangible assets at the price below their market value and pay dividends immediately. This shareholders behaviour is also referred as under-investment.

Examples above illustrate that when the possibility of financial distress is high shareholders tend to benefit at the expense of debt holders. However, if security holders predict that a company may gamble for resurrection, they pay less for risky securities. This implies that the company receives fewer funds for their investment and we may state that the amount of agency costs rises as long as the firm�s debt increase.

Despite of agency costs associated with leverage, there are some circumstances when benefits from the debt may be obtained. Leverage reduces free cash available and managers are prevented from building empires and wasteful spending. Debt may also stimulate managers to launch greater strategies, but too much debt may encourage managers to use their limited liability option.

The OECD findings regarding risk management practices state that, with some exceptions, risk management was not enough regulated by existing corporate governance standards. Thus, the most credible reason to explain the cause of the financial crisis is inadequate risk management according to the chosen strategy. However, risk may be managed if specific risks that influence business are well understood and they are assessed independently from profit centres.

Good corporate governance practices also indicated the importance to consider strategy and risk management issues simultaneously at the board level and for the purpose of increased transparency suggested a public disclosure of business risk factors.

2.3. A review of risk management practices in US and European banks

According to the corporate governance study in 25 largest European banks, the Head of Internal Audit was elected and dismissed by the board in fourteen of the peer banks. The same investigation revealed that there was a requirement that the Audit Committee should collaborate directly with internal auditors on a regular basis in thirteen peer banks. It was also disclosed the demand to meet with external auditors at least once a year in 60% of the peer banks. However, despite of maintaining independent audit practices and acknowledgement that identifying and managing risk is one of the most important boards� functions, the study disclosed weaknesses in risk management systems. It states that �only one third of our interviewees were confident that the strategy and planning departments of their banks had a detailed understanding of their companies� risk measurement methodology�[20].

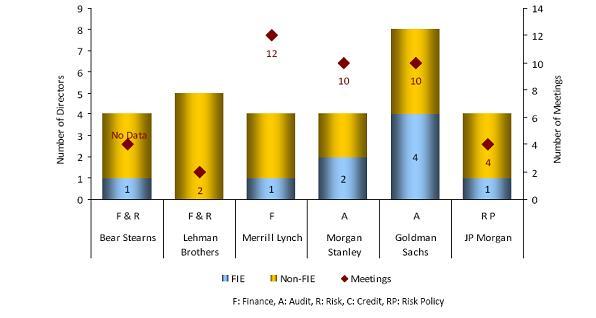

According to the corporate governance study of the six US banks, risk management practices are contrary to the European. Analysis revealed that only the JPM from the six peer banks had clearly defined obligations for the board to oversee risk management. This observation implies that risk was not sufficiently discussed at the board level. In the LEH�s case, credit and market risks were considered in the Finance Committee twice in 2007; similarly the Risk Committee in the BS was established only few months before the failure of its two hedge funds. More information about the Risk Committees meetings and directors� finance experience is provided in figure 6.

Investigation of risk management in the six US banks also revealed that all of the banks had formal sophisticated risk management systems. However, risk management issues did not reach boards. Moreover, risks those banks �were facing by continuing to leverage their balance sheets, expanding their trading books and using tools such as VaR to measure risks in instruments whose liquidity and credit risk profiles made them unsuitable for VaR analysis�[21].

Figure 5: Risk committee(s) meetings are FIE as a percentage committee size in 2007[22]

It is well known that funding liquidity risk and systematic risk are specific in banking sector and failures to manage them increase vulnerability of global economy.

Analysis of strategies that banks implemented during the past decade indicates clearly why risk management cannot be considered separately from strategic decisions. The start of the financial crisis laid down in the macroeconomic conditions. Favourable circumstances such as �unusually low real interest rates, easy credit conditions, low volatility in financial markets and widespread increases in asset prices�[23] encouraged banks to launch aggressive strategies. �Rapid development of securitisation and wholesale funding�[24] promised higher returns and demand to satisfy additional lending led to the increase of banks� leverage.

Debt obligations considered as positive financial decision because interest expenses are tax deductable and cash flows to all investors are higher with leverage. Consequently, �the total value of the levered firm exceeds the value of the firm without leverage due to the present value of the tax savings from debt.�[25] Thereby, it can be stated that the maximum benefit from leverage is obtained while interest expenses are equal to EBIT. However, increased debt raises the probability of bankruptcy and additional value generated from the interest tax shield is offset by the costs of financial distress. So, advantage of debt holds as long as company receives stable cash flows and has enough tangible assets.

The threat of banks� bankruptcy emerged when lending was still growing despite of the worsen credit repayments. Thus, revenues declined as expected incomes were not received. The other reason of the fail may be explained by inadequate source of funding. As long as households� savings rate declined banks start raising funds from international financial markets to satisfy the demand of growing loans. However, short term external funding to support long term loans also led to liquidity problems.

Moreover, it appeared that collateral assets were overvalued and banks started to write-off them. The probability of the default increased as market value of banks� assets declined compared with their liabilities. The bankruptcy could be avoided by raising equity capital. However, as the biggest part of banks encountered with the same problems �financial markets became dysfunctional and the solvency of large parts of the global banking system was challenged�[26].

Critical circumstances were mitigated by government interventions, so that banks had accession to sufficient capital, their losses were absorbed, market confidence was restored and banks started lending again.

According to the collapse of stability in banking sector, risk management proposals are considered as primary in the Walter Review. It was proposed that boards should be responsible for assessment of company�s risk appetite and tolerance as well as reassurance of well functioning risk management system. Additionally, in order to increase risk management efficiency, establishment of Risk Committee, whose functions were separated from Audit Committee, was suggested and requirements for the CRO to assess company�s wide-range risk independently were proposed.

The Walter Review also provides specific recommendations regarding risk strategy and risk factors disclosure. It is noted that corporation�s risk strategy should include strategies for capital and liquidity management. Recommendations for annual risk report suggested assessment of both banking and trading book exposures, evaluation of risk management effectiveness and disclosure of information regarding the scope and outcome of the stress-testing programme. It is expected that risk adjusted strategic management will prevent from excessive risk taking.

The Turner Review supplements recommendations for increased financial stability. It is proposed to strengthen regulations on capital, liquidity and accounting. The review states that risk management should be comprehensive and involve both macro risk and micro risk assessment. Moreover, the importance of regulations quality was emphasized. It was noticed that requirements in regulations should be set in such a way that leads to the companies� enhanced performance.

Additionally, the financial crisis revealed importance of cross-border banks supervision and improved global collaboration. So, the Turner Review recommended to establish European body which would control macro environment risk and supervise cross-border financial institutions as well as smooth business cycles and help to resilient from liquidity shocks.

As long as excessive cash flows are generated, the conflict of interests between managers and investors arise regarding retained earnings, payout policy and managers� compensation. Company�s performance highly depends on managers� efforts, however compensations reduce the amount of retained earnings that could be invested in positive NPV projects or be paid out for shareholders.

In this instance, flexible response in current circumstances required. Excessive cash flows may be used to reduce leverage and prevent from financial slacks. It also could reduce costs of rising capital for the future investment opportunities and prevent from financial distress costs. But on the other hand, excessive cash flows increase company�s taxes and encourage inefficient fund allocations as well as excessive executive perks.

The threat for shareholders arises, when there is no adequate power balance between managers and shareholders� representatives. Most often allocation of excessive cash flows is set by managers, who care about their job security and have incentives to maintain control over excessive cash. As the managerial entrenchment theory of payout policy states, managers �pay out cash only when pressured to do so by the firm�s investors�[27].

It is impossible to write contracts that reflect all obligations of the parties concerned. Moreover, financial commitments defined through remuneration may have two implications. Incentive system may encourage managers to take excessive risks and increase probability of bankruptcy. But it also may reduce principal-agent problems if managers� awards are aligned with long term shareholders� value growth.

According to the CEOD reports, the remuneration and incentive systems are too much influenced by the executives and the boards have little abilities to evaluate performance independently. When there is a lack of managers� control shareholders� interests may be violated. Thus, serious weaknesses in corporate governance standards regarding remuneration should be eliminated by enhanced independent directors� responsibilities to define company�s remuneration and incentives policy.

Reports also stated that broadly used stock price of the company was not straight measure to reflect specific firm�s performance. As firms� goals and activities are unique, distinctive measures require to be taken to evaluate personal achievements. As well as appropriate incentives should be used to align managers performance with shareholders� needs.

As investigation of global practices showed, applied remuneration schemes were too complicated and incentives often encouraged excessive risk taking. Thus, it was proposed to clarify incentive systems and set executives� compensation on measures that reflect realization of long term goals.

In order the transparency was increased, suggestions that shareholders should approve remuneration policy on annual meetings were expressed as well as requirements to publish the remuneration program that reflects the total costs, specified performance criteria and risk elimination actions were proposed. It is expected that these recommendations will increase shareholders� awareness about the remuneration policy and will let them to express their position by exercising their voting rights.

Additionally, the Financial Stability Forum published The Principles for Sound Compensation Practices[28] that are adjusted to financial institutions. These recommendations based on sound practices should help financial institutions to reduce principal-agency problems.

3.3.A review of remuneration practices in US and European banks

According to the corporate governance study in 25 largest European banks, the twenty four of the peer banks had the Remuneration Committee.

The research showed that mainly non-executive directors were assigned to the Remuneration Committees and on average 84% of them were independent.

It was also disclosed that in 29% of all the peer banks, the Remuneration Committees were delegated to make decisions regarding the remuneration of executive director. In other cases, the Remuneration Committees provided only suggestions.

As the European banks practice showed, the Remuneration Committees supervised the remuneration process quite independently however, the biggest part of them where not responsible for the remuneration policy.

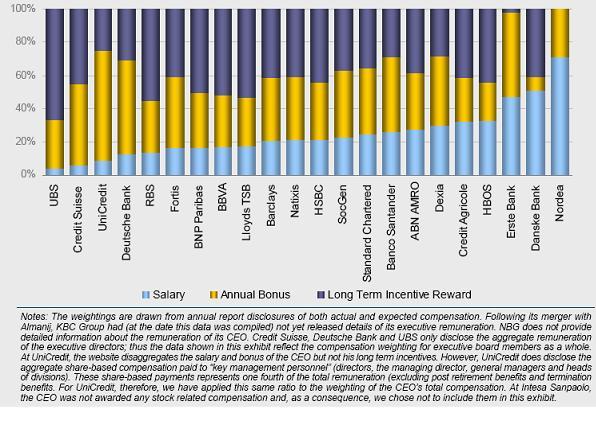

According to the research of the remuneration structure in European banks (see figure 7), the banks applied different compensation approaches. �In some countries it is now commonly accepted as �best practice� that variable (�at risk�) compensation should constitute the bulkof executive compensation. By contrast, in other jurisdictions (notably the Scandinavian countries), the preference is for a much higher ratio of fixed to variable compensation�[29].

Figure 6: The relative weighting of the CEO compensation (excluding pension and benefits)[30]

The study of 25 largest European banks also revealed that �the average weighting is: Salary (24%), Annual Bonuses (37%), Long Term Incentive Rewards (40%)�[31]. As basic salary presents the lowest weight in the remuneration structure, this implies that remuneration systems in European banks are flexible and easily adjusted to the companies� performance. Moreover, the highest weight in the remuneration structure is comprised of the long term incentive rewards. That shows high managers� incentives alignment with the long term shareholder�s value maximization. Analysis provided below additionally proves the remuneration adjustability to the long term companies� performance.

According to the structure of the short term variable compensation, the average annual maximum bonus presented 174% of executive director�s basic salary. Additionally, eleven of the peer banks disclosed that they used both quantitative and qualitative approaches to align performance to the remuneration.

The research on the structure of the long term variable compensation revealed that preferences for restricted share awards was growing and approximately one third of the peer group relied on share or cash compensation and did not allocate any stock options to heir senior managers. Moreover, it was indicated that award of the long term variable compensation depended on the performance conditions and valuation of the results involved share price, EPS, ROE or EVA measures.

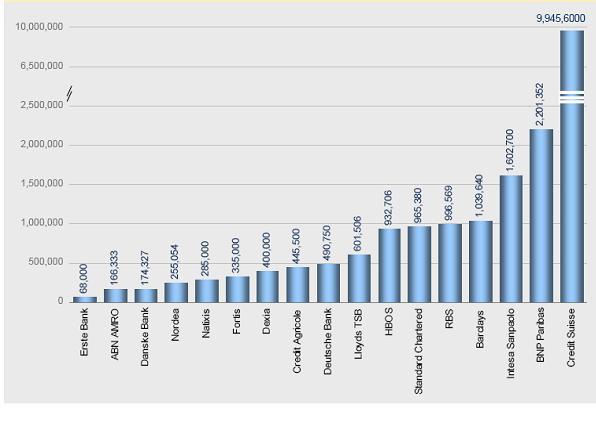

According to the study of European banks, fees paid for non-executive directors also varied wide. It was stated that �the average additional fee (as a percentage of the basic fee) for committee memberships is: 36% for Audit Committee membership (and 64% for committee chairmanship); and 28% for Remuneration Committee membership (and 41% for committee chairmanship)�[32]. Data provided above shows that basic fee for non-executive directors equal to the third of the total remuneration. This implies that remuneration systems are aligned with companies� performance. Comparison of different annual compensation of non-executive Chairmen is illustrated in figure 8.

Additionally, the study of European banks showed that non-executive directors held shares of the companies they represent. This practice shows that non-executive directors� interests are close to the other shareholders� long term needs.

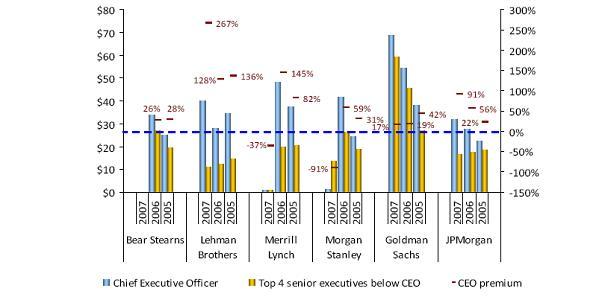

A study on the six US banks revealed that remunerations for executives were relevant to companies� performance as well. Figure 9 provides information about executive remuneration versus the ROE in 2007. However, �top executive salaries, averaging only 2% of annual total compensation across the whole peer group in recent years, are very low and contrast with the European salary average of 20‐35% of total remuneration�[33]. This fact implies that the remuneration system in US banks is less flexible to reflect the performance of company compared to the European banks.

Figure 7: Total annual compensation of non-executive Chairmen.[34]

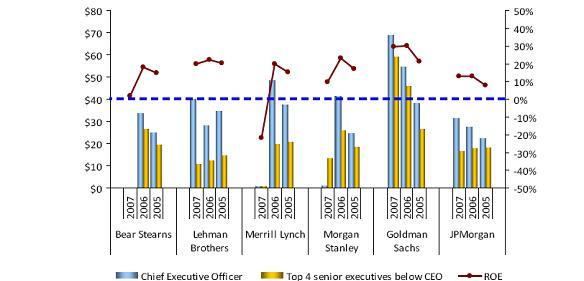

Figure 8: Top 5 executive remuneration versus ROE in 2007.[35]

Additionally, a research was made to compare differences of compensations between the chief executive and the four highest-paid senior executive officers. As data in figure 10 shows the highest differences appeared in the LB and the ML that indicates entrenched the Chief executives� powers.

Figure 9: Chief executive pay versus top 4 senior executive pay.[36]

The Walker Review suggested that the Remuneration Committee should set remuneration policy for the overall firm basis. This recommendation clearly defines the scope of responsibilities for the Remuneration Committee and implies that strategic decision regarding remunerations should be approved by shareholders� representatives.

There was noticed that company�s �high end� employees and their activities may have particular effect on company�s risk exposure, so boards should oversight the outcome of the incentives they set in the remuneration policy. The threat of diminished shareholders� worth may emerge from executives� excessive risk taking. So, requirements to use risk adjusted, deferral incentive payments systems that are aligned with the firm�s long term performance are highly recommended.

In order to protect company�s sustainability the collaboration between the Remuneration Committee and the Risk Committee was proposed. The aim of this collaboration is to set objectively risk adjusted performance goals and incentive packages.

The Walker Review also proposed to publish details about the annual assignments of the remunerations that exceed �1 million. It was also recommended that if the annual remuneration report gets less than 75% approval, the chairman of the committee should be re-elected. It is expected that implementation of these recommendations will increase shareholders� awareness about the remuneration decisions and enhance the chairman�s responsibility.

Additionally, in order good remuneration practices were start implemented, the FSA published the policy statement: Reforming remuneration practices in financial services[37].

As long as different interest between shareholders and managers frustrates company�s performance it may be declare that rewarding the CEOs by companies� shares will encourage managers to perform in behalf of other shareholders. However, investors tend to diversify their investment portfolios so the shareholders also try to avoid their dependence on one company.

Additionally, it may seem that combined the CEO/Chairman role should safeguard shareholders rights and interests, especially when the CEO have large amount of share holdings. But it is hard to expect efficiency when implementation and control functions are assigned to the same person.

However, principal-agent problem may be reduced by exercising shareholders� rights. This mostly depends on the investor�s type.

When investors are small and dispersed managers do not feel responsibility to be accountable for shareholders. Most often small shareholders cannot cooperate their actions and effect company�s decisions. So, agency problem solving is relied on the market control mechanism. If corporation perform well investors purchase shares of well managed corporations, and company�s share price is rising. And contrary, the share price is falling when investors find more attractive investment opportunities and sell company�s shares. Thus, market evaluation of the company�s performance creates incentives for managers and boards of directors to meet interest of their shareholders. The reason may be explained as following.

When share price of the company decline substantially, a new owner, who thinks that the firm could be managed more efficiently may launch a raid, buy company�s shares and dismiss former managers. However, takeovers are costly. If new investor has incentives to buy company and improve its performance, current shareholders do not have incentives to sell shares as they expect the share prices to rise after the reorganization. If takeover occur to be too expensive for a new investors they refuse to continue takeover process.

Eventually, large shareholders have a powerful tool to eliminate agency costs if they actively supervise how efficient their wealth is managed. Shareholders may use their rights to control how managers� performance is aligned with shareholders� long-term value maximization needs.

Global practice showed that when managers had substantial part of their wealth invested in business they ran, it did not guaranteed business sustainability. Intuition, that managers, who also are significant owners of the company, look after the performance of the company more carefully is misleading if managers perceptivity regarding business is short-term.

Moreover, past events disclosed, that the equity share of institutional investors increased, howevershareholders tended to be passive regarding initiatives to change business decisions. Most often they just responded to the company�s performance. Thus, it was suggested to enhance shareholders involvement in decision making. This proposal should encourage managers to perform according shareholders� long term needs.

It should be noticed that enhanced shareholders participation in companies� strategic affairs could increase conflicts of interests. So, efficient shareholders and managers collaboration could be reached only by constructive debates. In order the higher productivity of discussions was reached, individual shareholders were encouraged to act together providing suggestions.

Additionally, the CEOD reports disclosed that there are significant weaknesses in regulations regarding exercising shareholders� voting rights. It was also mentioned the lack of technical readiness to facilitate flexible voting such as electronic voting. Hence, it was proposed to take appropriate measures in order the obstacles due to fulfilment of shareholders� rights were removed. Thus, it is expected that shareholders will monitor business performance actively by using their rights to participate in decision making.

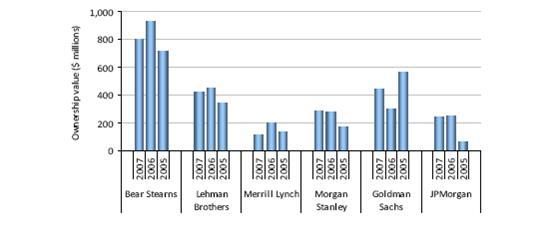

The research of corporate governance in the six US banks showed that executives� long-term interests were aligned with those of shareholders. It is observable from the CEOs ownership in the companies they managed. Long term serving, especially in the BS and the LEH cases, let the CEOs to gain sufficient part of the total company�s shares and become significant owners. Thus, the assumption that their at-risk wealth was high could be made (see Figure 11).

Figure 10: Chief executive officer total at-risk wealth.[38]

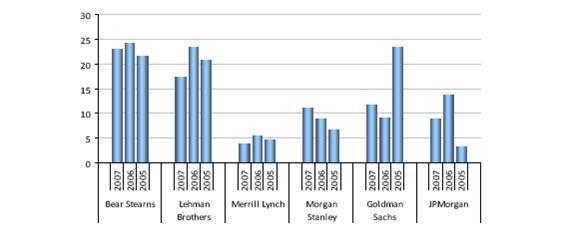

However, it was also mentioned in the six US banks study that focus on share price is not appropriate indictor to measure alignment with long-term shareholders worth. So, additionally to the size of the individual stock‐related wealth investigators tried to find a relationship between an executive�s stock holding and his personal wealth. Such indicator seemed to be a reliable foundation to state that high level of executive�s stock holdings compare with their total personal wealth is a strong incentive to perform in the long-term interest of other shareholders. The ratio of total at-risk wealth over income was determined as following: �Not having access to individual measures of wealth 25 for the chief executives of the banks, we used as a proxy for �expected wealth�, the average annual income in the preceding five years. We estimated total annual income as the sum of annual compensation awards and total dividend income from ownership of company stock. The ratio of total at‐risk wealth over income, labelled personal risk exposure indicator (PREI), is calculated by dividing: Total at‐risk wealth (as defined above) by Average annual income in the preceding five years.�[39] The CEO personal risk exposure indicator is provided in figure 12.

Figure 11: CEO personal risk exposure indicator.[40]

The other aspect of entrenched management in strategic decision making and a lack of accountability may be checked by analyzing voting systems. The �plurality�[41] voting system that was prevailing in US may be mentioned as a reason of the boards lack accountability to the shareholders. The study of the six US banks revealed that �only the BS maintained the plurality system until the time of its demise. All the other banks amended their Articles to switch to various forms of majority voting for directors in 2006 and 2007�.[42]

Additionally, it was noticed the increase of institutional shareholders in Europe. So, it is expected that their supervision of banks by exercising voting rights will have a significant contribution to the protection of shareholders� long term business value maximization needs.

According to the Walker Review the development of regulations that encourage institutional investors and fund managers actively participate in monitoring of corporations� performance is required. Large shareholders� involvement into the companies� affairs and stimulation to exercise shareholders� rights are important devises to protect investors� interest due to companies� sustainable, long term value creation.

Thus, in order the best practices regarding the fulfilment of shareholder�s rights were implemented successfully and managers� control was strengthened, a recommendation to prepare the code on the responsibilities of institutional investors was proposed. It was suggested to separate extended regulations on the implementation of shareholders� rights from the Combined Code and call it as the Stewardship Code.

It was also emphasized that institutional investors and fund managers should collaborate by exercising their shareholders� rights. In this instance, it is expected that active shareholders� position should affect the sustainability of the performance of companies.

Moreover, a provision that obliges institutional investors or fund managers to disclose whether they commit to the Stewardship Code was suggested. If institutional investors or fund managers do not meet the requirements based in the Stewardship Code, they are required to disclose the alterative business models they apply to manage funds. Thus, in any case shareholders� involvement in monitoring companies� performance should be strengthened.

The Global Financial Crisis and growing complexity of financial markets encouraged authorities and other voluntary initiatives to increase corporate governance standards.

According to the business globalization, internationally discussed corporate governance problems and suggestions to tackle them are similar to those proposed to apply in UK financial institutions. Differences between recommendations occurred due to particular UK authority mechanism and specific features of financial industry. So, the most important factors that help to eliminate principal-agent problems by legislations may be summarized as following:

� boards� independency and qualification,

� risk adjusted strategic finance management,

� remunerations� alignment with long-term rather than short-term performance,

� and exercising shareholders� rights.

However, human behaviour should be mentioned alongside. People are not robots that act under anticipated instructions. So, mostly human behaviour, not legislation, creates or destroys shareholders wealth. Moreover, despite of turbulent environmental conditions, investors� behaviour remains the same. They seek investment opportunities that promise highest possible returns according to their risk preference.

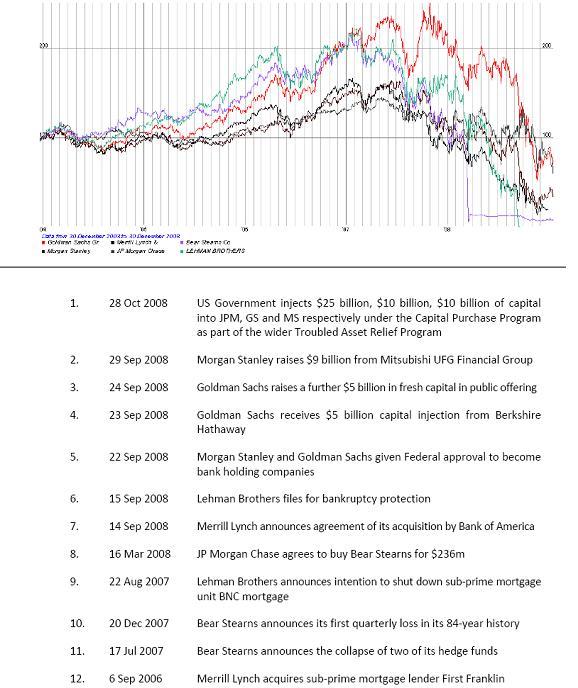

Timeline of key events those were significant for 3 survived and 3 departed US banks[43]

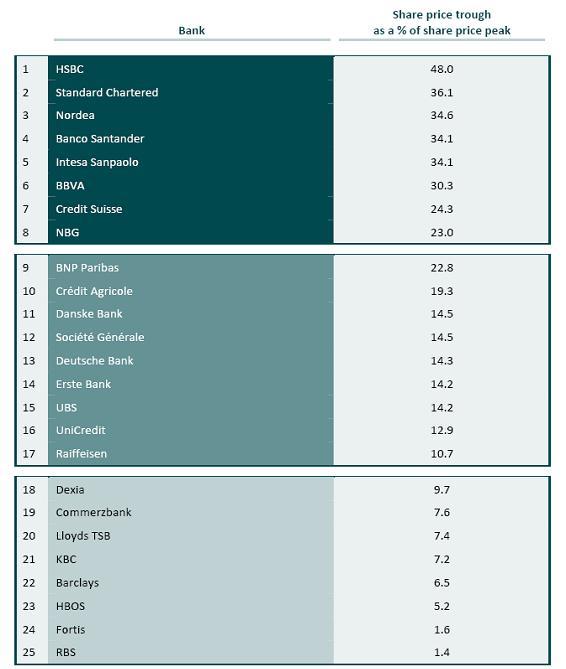

The list of 25 largest European banks[44]

1. BIS: II. The global financial crisis � BIS 79th Annual Report, June 2009 (at http://www.bis.org/publ/arpdf/ar2009e2.pdf)

2. Derek Higgs, Review of the role and effectiveness of non-executive directors, 2003 January, (at http://www.berr.gov.uk/files/file23012.pdf)

3. Financial Reporting Council, 2009 Review of the Combined Code: Final Report, December 2009 (at http://www.frc.org.uk/images/uploaded/documents/2009%20Review%20of%20the%20Combined%20Code%20Final%20Report1.pdf)

4. Financial Reporting Council, The Combined Code on Corporate Governance, June 2008 (at http://www.frc.org.uk/documents/pagemanager/frc/Combined_Code_June_2008/Combined%20Code%20Web%20Optimized%20June%202008(2).pdf)

6. Members of the FSF Compensation Workstream: FSF Principles for Sound Compensation Practices, 2 April 2009 (at http://www.financialstabilityboard.org/publications/r_0904b.pdf)

7. Nestor Advisors Ltd: Board profile, structure and practice in large European Banks. A comparative corporate governance study. Executive Summary, 2009

(at http://www.nestoradvisors.co.uk/fileadmin/user_upload/articles/ExecSum.pdf)

8. Nestor Advisors Ltd: David Ladipo, Stilpon Nestor. Bank Boards and the Financial Crisis. A corporate governance study of the 25 largest European banks, May 2009 (at http://www.nestoradvisors.co.uk/fileadmin/user_upload/articles/Intro.pdf)

9. Nestor Advisors Ltd: Governance in Crisis: A comparative case study of six US investment banks, NeAd Research Note 0109/April 2009 (at http://www.nestoradvisors.co.uk/fileadmin/user_upload/articles/USBank09.pdf)

10. OECD: Corporate Governance and the Financial Crisis: Key Findings and Main Messages, June 2009 (at http://www.oecd.org/dataoecd/3/10/43056196.pdf)

11. OECD: OECD Principles of Corporate Governance, 2004 (at http://www.oecd.org/dataoecd/32/18/31557724.pdf)

12. OECD: The Corporate Governance Lessons from the Financial Crisis, 2009 (at http://www.oecd.org/dataoecd/32/1/42229620.pdf)

13. Response from the Financial Services Authority (FSA) to the Treasury

Committee report on Banking Crisis: Regulation and Supervision, 6 November 2009, (at http://www.parliament.uk/documents/upload/FSAresponse.pdf)

14. The Financial Services Authority: Consultation paper 09/30 *** Capital planning buffers, December 2009, (at http://www.fsa.gov.uk/pubs/cp/cp09_30.pdf)

15. The Financial Services Authority: Discussion paper 09/2 A regulatory response to the global banking crisis, March 2009, (at http://www.fsa.gov.uk/pubs/discussion/dp09_02.pdf)

16. The Financial Services Authority: Discussion paper 09/2 newsletter. The Turner Review and Discussion Paper 09/2 - a regulatory response to the global banking crisis, March 2009, (at http://www.fsa.gov.uk/pubs/discussion/dp09_02_newsletter.pdf)

17. The Financial Services Authority: Financial Risk Outlook, 2009, Page 8 (at http://www.fsa.gov.uk/pubs/plan/financial_risk_outlook_2009.pdf)

18. The Financial Services Authority: Policy statement 09/15. Reforming remuneration practices in financial services. Feedback on CP09/10 and final rules, August 2009 (at http://www.fsa.gov.uk/pubs/policy/ps09_15.pdf)

19. The Financial Services Authority: Policy statement 09/16. Strengthening liquidity standards including feedback on CP08/22, CP09/13, CP09/14, October 2009, (at http://www.fsa.gov.uk/pubs/policy/ps09_16.pdf)

20. The Financial Services Authority: The Turner Review A regulatory response to the global banking crisis, March 2009 (at http://www.fsa.gov.uk/pubs/other/turner_review.pdf)

21. The Walker review secretariat: A review of corporate governance in UK banks and other financial industry entities. Final recommendations, 26 November 2009 (at http://www.hm-treasury.gov.uk/d/walker_review_261109.pdf)

[4]Financial Reporting Council, 2009 Review of the Combined Code: Final Report, December 2009 (at http://www.frc.org.uk/images/uploaded/documents/2009%20Review%20of%20the%20Combined%20Code%20Final%20Report1.pdf); The Financial Services Authority: Consultation paper 09/30 *** Capital planning buffers, December 2009, (at http://www.fsa.gov.uk/pubs/cp/cp09_30.pdf); The Financial Services Authority: Policy statement 09/15. Reforming remuneration practices in financial services. Feedback on CP09/10 and final rules, August 2009 (at http://www.fsa.gov.uk/pubs/policy/ps09_15.pdf);

The Financial Services Authority: Policy statement 09/16. Strengthening liquidity standards including feedback on CP08/22, CP09/13, CP09/14, October 2009, (at http://www.fsa.gov.uk/pubs/policy/ps09_16.pdf); The Financial Services Authority: The Turner Review A regulatory response to the global banking crisis, March 2009 (at http://www.fsa.gov.uk/pubs/other/turner_review.pdf); The Walker review secretariat: A review of corporate governance in UK banks and other financial industry entities. Final recommendations, 26 November 2009 (at http://www.hm-treasury.gov.uk/d/walker_review_261109.pdf)

[41]In plurality voting, the nominees for available directorships who receive the highest number of affirmative votes cast are elected irrespective of how small the number of affirmative votes is in comparison to the total number of shares voted. Majority voting requires that a nominee receives the affirmative vote of a majority of the total votes cast for and against such nominee in the election.